Be active for passive income: How to plan around the new small business tax changes

By Mike Magreehan

Features Business Finance accountant accounting business owner taxes business tax help chiropractic how to do taxes tax Photo by Helloquence on Unsplash

Photo by Helloquence on UnsplashThe government enacted a number of new tax changes last year that could dramatically impact the bottom line of many Canadian businesses, including incorporated professionals – chiropractors, doctors, lawyers and accountants. In this article, we will examine an area that has received considerable attention from small businesses and industry groups: the potential loss of some (or all) of the small business deduction (SBD).

Although we are well into 2019, there are some legitimate tax planning opportunities worthy of consideration now that may lessen or even eliminate the negative impact of these tax changes on you going forward.

After salaries, dividends and expenses have been paid, incorporated professionals have enjoyed investing their retained earnings tax-efficiently inside their corporation. If you are going to withdraw the earnings each year to fund current lifestyle needs, then the loss of the SBD may not be material. However, professionals electing to invest inside their corporation could enjoy a significant tax deferral by simply leaving funds in their corporation for investment

purposes.

The old rules allowed a lower tax rate on the first $500,000 of passive investment income, but along with a host of other new tax measures, one aspect of particular concern is the gradual loss of the SBD, as the $500,000 limit no longer fully applies.

The changes are meant to eliminate tax benefits achieved when active business income is taxed at low rates and reinvested passively within a corporation. From the government’s perspective, an unfair tax advantage existed for business owners. Since corporations generally have access to greater pools of after-tax capital, the corporation could invest those dollars and earn passive investment income and compound those pools of capital in order to withdraw them tax-efficiently in the future.

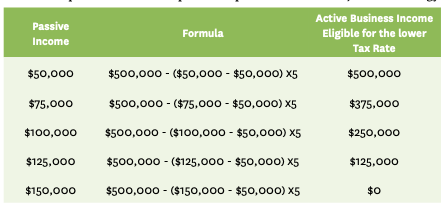

Under the new rules, passive income earned inside a corporation can lower a corporation’s SBD limit. This reduction begins when a corporation earns $50,000 of passive income in the prior year. Specifically, the SBD will be reduced by $5 for every $1 of investment income above the $50,000 threshold. As such, the SBD would be completely eliminated if the combined investment income of your corporation (and associated corporations) for the taxation years that ended in the preceding calendar year is over $150,000.

To illustrate, if your corporation earned at least $50,000 of passive income last year, then some (or all) of the income that would have qualified for the low SBD corporate tax rate (12.5 per cent for Ontario) would be taxed at the higher, general corporate tax rate this year (26.5 per cent in Ontario). As you can see, losing the SBD is a tax to the business owner, as this means higher taxes which translates into less capital to invest. The impact of these measures will only compound over time.

Passive investing – Planning strategies with your corporate investment portfolio

If you maintain an investment portfolio within your corporation and you are nearing or exceeding the $50,000 passive income threshold, enacting strategies to intentionally reduce passive income within your corporation may lessen the impact of the changes on you. Let’s face it, you work hard for your patients, your family and your money. There are several ways to do this and the following strategies are considerations to help you reduce the negative consequences to your SBD limit in 2019 and beyond.

Investment strategies

Capital gains continue to be one of the most tax-advantaged ways to invest, both personally and corporately. Compared to ordinary investment income that is fully included in the passive income calculation, only half of the realized capital gains are included. So, it would take $100,000 of realized capital gains to generate $50,000 of passive income that could be counted toward the SBD test.

You might decide to invest corporate dollars in growth stocks or funds, where interest and dividend income are negligible, that will have a smaller impact on the SBD limit. As those securities appreciate over time, you may then time profit-taking in a year where it is most favourable for you – i.e. when passive income is below the $50,000 threshold. Likewise, if your current year’s passive income is high enough that it will fully eliminate next year’s SBD, consider crystalizing additional capital gains now, which may allow the negative impact of realized capital gains on the SBD to be lumped into one year in order to restore your SBD for the following years. Additionally, you may wish to trigger capital gains and losses in the same year, because capital losses cannot be carried forward to future years for the purposes of reducing passive income.

A special tax-efficient structure of mutual funds, known as Corporate Class funds, is a legitimate option for Canadians because investment income earned can be deferred and therefore compounded within the Corporate Class fund tax-favourably. These funds have been a popular option for decades and are finding renewed intrigue resulting from the new tax rules.

Real Estate Investment Trusts (REITs) and another special mutual fund structure, known as T-Series funds, pay a regular income stream which is mainly the return of capital. A return of capital is not taxable in the year that it is received. Rather, it proportionately reduces the adjusted cost base of the investment so that when the investment is ultimately sold, a capital gain is generated. Again, you may effectively time the disposition of the securities which will provide you with more planning flexibility.

Corporate-owned tax-exempt cash value insurance

ou may choose to invest corporate dollars within a tax-exempt life insurance policy. Tax-exempt policy values can compound significantly over time and are not included in the passive income calculation. The corporation would own the insurance policy that insures the life of the business owner (or a related/connected individual) and upon the life insured’s passing, the insurance proceeds would be received tax-free by the corporation and then paid out largely (if not entirely) tax-free as a capital dividend to the intended beneficiaries.

The policy’s dividends and growth are tax-sheltered within the life insurance policy and do not form part of the passive income calculation.

There are sound strategies whereby you may access your policy’s cash value in the future while you are alive, such as supplementing retirement income, but if cash values are not accessed properly, the passive income test may be triggered.

Where the policy will be used for long-term legacy and estate planning purposes, such as a tax-free payout at death to your corporation as beneficiary. The new shareholder(s), i.e. the family, would elect a payout via the Capital Dividend Account to the ultimate intended beneficiaries (i.e. your spouse and children). This strategy can be a highly lucrative vehicle for maximizing your family’s overall wealth and well-being.

Maximize RRSP/TFSA accounts

Consider paying a sufficient salary to maximize your RRSPs and TFSAs. The corporation would receive a tax deduction for the salary payment, which in turn can reduce your general corporate tax rate. Invested wisely, income and growth from RRSP and TFSA will also compound tax-sheltered and given sufficient time, they can outperform corporate investing. Reasonable salaries may also be paid to family members who work in the business to allow them to contribute to their RRSPs and TFSAs. Lastly, removing funds from the corporation that would otherwise be invested could reduce the chance of losing the SBD in future years.

Individual pension plans

An Individual Pension Plan (IPP) is a defined benefit pension plan created for the business owner, incorporated professional and spouse if employed by the corporation. They offer far greater contributions compared to RRSPs, can hold a wide range of investments, have the ability to top up on a tax-deductible basis if they fail to achieve a 7.5 per cent return and are fully creditor proofed. IPPs have been growing in popularity amongst professional business owners as a result of the tax changes. Often touted as super-sized RRSPs, IPPs are a specialized solution and can be suitable under the right circumstance. Although they are more complicated to set up and administer, as an actuary is needed to determine contribution limits and requirements, they can easily make a great deal of sense.

Contributions to the IPP provide tax deductions to the corporation, which can keep business income below the small business threshold and for older businesses there can be a sizable past service deduction to backdate the plan to when the owner started the corporation. Actuarial and investment management fees are tax-deductible. Furthermore, investment income earned within an IPP is the individual’s and is therefore not a corporate asset, so it will not add to the passive income calculation. IPPs have ongoing administration costs and are not suitable for everyone, but for those with excess cash flow, they can be an effective savings tool. Working with a qualified financial professional to determine suitability and investment strategy is wise.

Conclusion

Although corporate investment income is considered passive, the new tax changes require some active planning. Navigating tax policy is an ongoing process. Responsibly evaluating and maximizing available opportunities is necessary to ensure your wealth strategies are intact.

Chiropractic professionals who are busy running a successful practice should seek guidance from a qualified team of financial professionals who offer non-biased, fully-independent advice and who have the depth of resources to assist you through all of life’s stages.

Mike Magreehan, is BBA (Hon), CFP® is an Investment and Insurance Advisor with Canaccord Genuity Wealth Management in Waterloo, ON. Mike welcomes your comments and questions at 1-800-495-8071 or mmagreehan@cgf.com. Visit LMwealth.com

Print this page